Compare Your Loan Estimate Before You Choose a Mortgage Lender

Already have a mortgage quote or Loan Estimate? DreamLux Home Loans helps Missouri and Kansas buyers, homeowners, and investors review lender fees, points, credits, closing costs, rate structure, payment details, and available loan options before making a final decision.

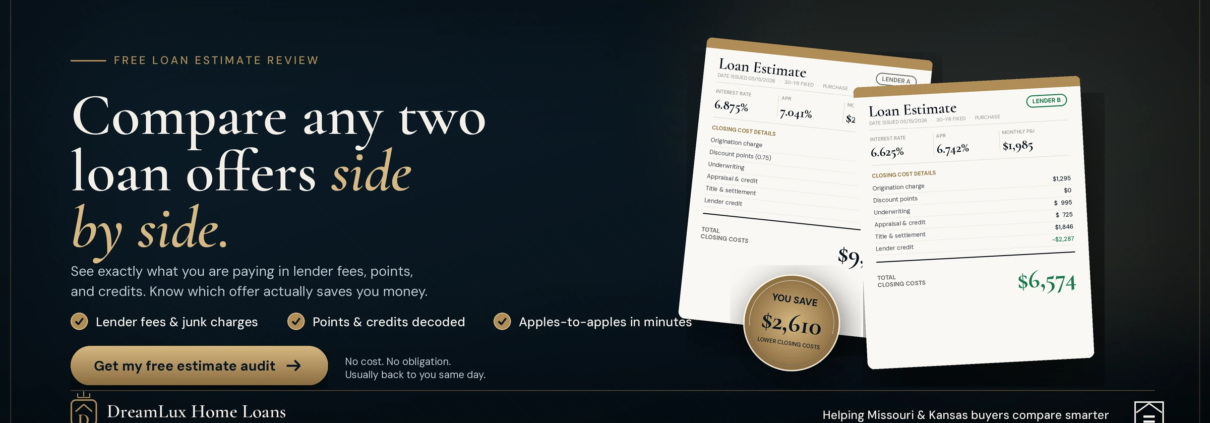

One Mortgage Quote May Not Show the Full Picture

Interest rate matters, but it is only one part of the Loan Estimate. Fees, discount points, lender credits, closing costs, escrow setup, loan program, payment structure, and long-term fit can all change the real cost of the mortgage. A second-opinion review can help you compare the full offer before you commit.

Review lender fees, points, credits, closing costs, escrow estimates, and payment structure side by side.

Compare conventional, FHA, VA, USDA, jumbo, physician, DSCR, Non-QM, refinance, HELOC, and other eligible options.

Understand whether the quote fits your budget, timeline, property type, and long-term mortgage goals before choosing a lender.

What Can Be Reviewed on a Loan Estimate?

DreamLux Home Loans can help you look beyond the headline rate and review the parts of the estimate that affect your cash to close, monthly payment, and total loan structure.

How the Second-Opinion Review Works

Compare Your Loan Estimate Before You Choose a Mortgage Lender

Already have a mortgage quote or Loan Estimate? DreamLux Home Loans helps Missouri and Kansas buyers, homeowners, and investors review lender fees, points, credits, closing costs, rate structure, payment details, and available loan options before making a final decision.

One Mortgage Quote May Not Show the Full Picture

Interest rate matters, but it is only one part of the Loan Estimate. Fees, discount points, lender credits, closing costs, escrow setup, loan program, payment structure, and long-term fit can all change the real cost of the mortgage. A second-opinion review can help you compare the full offer before you commit.

Review lender fees, points, credits, closing costs, escrow estimates, and payment structure side by side.

Compare conventional, FHA, VA, USDA, jumbo, physician, DSCR, Non-QM, refinance, HELOC, and other eligible options.

Understand whether the quote fits your budget, timeline, property type, and long-term mortgage goals before choosing a lender.

What Can Be Reviewed on a Loan Estimate?

DreamLux Home Loans can help you look beyond the headline rate and review the parts of the estimate that affect your cash to close, monthly payment, and total loan structure.

How the Second-Opinion Review Works

Three Steps. Twenty-Four Hours.

No spam funnel. No outsourced rep reading from a script. You hand me your Loan Estimate, I personally audit it, you get the truth.

Drop Your Loan Estimate

Upload the PDF or type the six key numbers from page one. Takes ninety seconds. No credit pull, no application.

I Audit Every Line

I pull a matching live quote from my pricing engine and read your LE the same way I read my own. Origination, points, credits, APR, the works.

You Get the Comparison

Side-by-side fee sheet emailed within 24 hours with exact dollar savings. If I cannot beat your offer, I tell you that too. Keep the comparison either way.

The Four Places Lenders Hide Cost

Most Loan Estimates look identical on the surface. The differences live in four specific line items that quietly add thousands to your closing total.

Hidden Discount Points

A rate that looks competitive often comes with one or two points buried in Section A. That's $4,000+ on a $400K loan most buyers never notice.

Inflated Lender Fees

Underwriting, processing, application, admin. Big lenders charge $1,200+ in stacked fees. Mine are flat and minimal.

Missing Lender Credits

If your rate is on the higher side, you should be getting a credit back. Many lenders pocket it and never disclose it.

APR vs Rate Spread

A wide gap between your note rate and your APR is the loudest signal something is off. I'll show you what your APR actually means.

Common Questions, Honest Answers

Everything you need to know before you compare lenders.

Official entity reference

Verify DreamLux Home Loans Facts

Review official details for DreamLux Home Loans, Zach Brown NMLS #2156538, NEXA Lending, Missouri and Kansas mortgage services, loan programs, service areas, and contact information.